School Finance University

Understanding How School Funding Works

School finance can be complex, but understanding how public schools are funded helps community members make informed decisions and better understand the financial challenges and opportunities facing school districts.

School Finance University is designed to provide clear, easy-to-understand information about Ohio school funding, local property taxes, school levies, state funding formulas, and district financial planning. Whether you're a parent, taxpayer, community member, or employee, these resources can help you better understand how Beavercreek City Schools is funded and how those resources support student learning.

Glossary

-

Abatement

Tax abatement is an exemption, in whole or in part, of real estate taxes incurred from new or

renovated improvements to a specific piece of property.Assessed Valuation

The percentage of valuation that is subject to taxation. For example, Class I and Class II property are assessed at 35%, personal tangible at 24% and public utility property at either 25% or 88%, depending on the type of utility.

Average Daily Attendance (ADA) Student membership calculation based on a district’s average attendance, as opposed to the number of students enrolled.

Average Daily Membership (ADM)

Number of students enrolled in a school district who are either in attendance or have an excused absence the first full week in October.

Biennium

Any two-year period, used mostly in school funding to refer to the two fiscal years that make up each state budget.

Bond Retirement Fund (Fund 002)

A fund provided for the retirement of serial bonds and short term notes and loans. All revenue derived from general or special levies, either within or exceeding the ten-mill limitation, which is levied for debt charges on bonds, notes, or loans, shall be paid into this fund.

Bond Levy

Property tax levies used to provide the local revenue for construction purposes. Proceeds from the levy are used to pay the principal and interest on construction bonds. Offered for a specified dollar amount and a specified period of time.

Categorical Expenditures

Categorical expenditures refer to expenditures required by school districts beyond the base-formula amount. Examples of categorical expenditures include special education, vocational education, gifted education, pupil based assessment, and transportation.

Commercial Activity Tax (CAT)

An annual business privilege tax measured by the gross receipts of businesses. Most companies doing business in Ohio will be subject to CAT, a broad-based, low-rate tax measured by gross receipts., CAT is levied at a rate of 0.26 percent on gross receipts in excess of $1 million.

Class I Property

Residential and agricultural property.

Class II Property

Commercial, industrial and all other property.

Continuing Levy

Levy proposing millage rate or school district income tax that is assessed indefinitely.

DeRolph I

March 27, 1997, Ohio Supreme Court decision where the court ruled, by a 4-3 vote, that Ohio’s school funding system was unconstitutional. The court allowed the state one year to craft a new funding system.

DeRolph II

May 11, 2000, Ohio Supreme Court decision where the court ruled, again by a 4-3 voted, that the new funding system created by the General Assembly in response to the DeRolph I ruling was still unconstitutional. The state was given until June 15, 2001, to again overhaul the funding system.

DeRolph III

Sept. 6, 2001, Ohio Supreme Court decision in which the court ruled, again by a 4-3 margin, though with a different group of justices comprising the majority, that the funding system incorporated in HB 94 would be constitutional pending a series of changes specified by the court. The state requested reconsideration of the decision.

DeRolph IV

On Dec. 11, 2002, the Ohio Supreme Court, in a 4-3 ruling, found Ohio’s school funding system once again unconstitutional and restated its decisions in DeRolph I and II, which required the state legislature to fix the school funding system. The court also relinquished jurisdiction over the case and essentially ended the lawsuit.

District Managed Student Activity Fund (Fund 300)

A fund provided to account for student activity programs that have student participation in the activity but do not have student management of the programs. This fund would usually include athletic programs but could also include the band, cheerleaders, flag corps, and other similar types of activities.

Dual Purpose Levy

Single ballot issue for both a permanent improvement levy or a bond issue combined with an operating levy. It may be continuing or limited. The ballot issue must state how much of the tax levy will be used for each purpose. A permanent improvement/operating levy may either be a property tax or a school district income tax, but a bond/operating levy must be a property tax.

Educational Service Center (ESC)

Local political subdivisions that are governed by publicly-elected boards of education (ORC 3311.055). ESCs provide services to area school districts including administrative, academic, fiscal, and operational support. All districts with an Average Daily Membership (ADM) of 16,000 or less are required to be affiliated with an ESC.

Effective Mills

The actual rate of taxation realized when the tax reduction factor reduces the taxes charged by a voted levy. It equals the taxes charged divided by the taxable value of the class of property against which they apply.

Emergency Levy

Limited levy proposed up to five years for a specific dollar amount. The millage rate required to produce the dollar amount changes on all types of property if property values change. Emergency levies may be renewed for the dollar amount originally requested.

Exempt Property

Real property not subject to taxation. Typically, exempt property is owned by federal, state or local branches of government, and religious or educational institutions.

Fiscal Year (FY)

Annual period used for government accounting purposes. Begins July 1 and ends June 30 of the next year. Named for the calendar year in which it ends (i.e., FY 2023 begins July 1, 2022 and ends June 30, 2023).

Forecast

According to Merriam-Webster Dictionary, forecast means to calculate or predict (some future event or condition) usually as a result of study and analysis of available pertinent data.

Floor

Rate below which voted mills will not be reduced under the property tax reduction factor. Established by the General Assembly, currently set at 20 mills.

Foundation Formula

Method of funding schools through a combination of state and local aid. Based on the ability of school districts to raise tax revenues as well as the state-determined minimum amount necessary per student to provide an adequate education.

Guarantee

Alternative calculation of state funding that insulates school districts from the effects of dramatic changes in school funding factors, such as property valuation or ADM. Guarantees are also often politically necessary when changes in state policy have disproportionate effects on different types of school districts.

Homestead Property

Property where the owner occupies the property as a residence. Such property qualifies for the additional 2.5% rollback. This term should not be confused with the homestead exemption that provides specific property tax relief to low-income elderly (65 and older) or disabled homeowners.

Incremental Property Tax Levy

Limited levy, with a maximum time of 10 years, that imposes additional millage, or a dollar amount or percentage increase, on a regular schedule throughout the life of the levy. Increments are imposed as the full voted millage, not as effective millage, giving a limited amount of growth in the levy. Up to five changes may be proposed during the life of the levy.

IDEA, Part B Fund (Fund 516) Grants to assist states in providing an appropriate public education to all children with disabilities.

Income Index

A component of the state funding formula that is an average of the median income index and the district three year average federal adjusted gross income per pupil compared to the statewide three year average federal adjusted gross income per pupil.

Inside Mills

Millage imposed by local governments without voter approval. Defined in the Ohio Constitution. Inside mills are not subject to the property tax reduction factor. Sometimes referred to as “unvoted mills."

Limited Levy

Levy proposing a millage rate or school district income tax hat is assessed for a specified period of time. A limited levy is eligible for renewal or replacement.

Median Income Index

A component of the state funding formula that compares the district median income to the statewide median income.

Millage

Factor applied to the assessed, a.k.a, taxable, valuation of real or personal tangible property to produce tax revenue. A mill is defined as one-tenth of a percent or one-tenth of a cent (0.1¢) in cash terms.

Operating Levy

Levy used primarily for district operating purposes, which can be either continuing or limited.

Outside Mills

Millage approved by voters. Outside mills are subject to the property tax reduction factor; sometimes referred to as “voted mills."

Permanent Improvement Fund (Fund 003)

A fund provided to account for all transactions related to the acquiring, constructing, or improving of such permanent improvements as are authorized by Chapter 5705, ORC.

Permanent Improvement Levy

Limited or continuing levy used for maintenance and repair of school property, and, in some limited circumstances, for renovation and building projects. This type of levy can be a property tax or an income tax.

Property Tax Reduction Factor

Sometimes referred to as the “HB 920” effect. An adjustment by which the taxes charged by voted mills in Class I and Class II real property are reduced to yield the same amount as those same mills yielded in the preceding year, exclusive of new construction. The reduction factor does not apply to inside mills or to voted mills charged against general and public utility personal property.

Property Tax Rollback

A percentage reduction in the taxes charged against all real property. The percentage equals 10% for all property and an additional 2.5% for owner-occupied residential property. The state reimburses schools and other local governments for the full amount of the rollback. The rollback applies after the reduction in taxes charged against real property as determined by the tax reduction factor. The 10% rollback for Class II commercial and industrial real property has been eliminated.

Public Utility Property

Tangible personal property used in the operations of a public utility company.

Qualifier

Minimum amount of millage required by state law for participation in the state foundation program. Currently set at 20 mills.

Real Property

Land and improvements to land such as structures or buildings. In Ohio, real property is divided into two classes: Class I (residential and agricultural property) and Class II (commercial, industrial and all other real property).

Reappraisal

Appraisal by the county auditor of the value of real property for tax purposes. It occurs every sixth year. Three years after each reappraisal, the county auditor adjusts appraised values based on recent sales of property in that county. This adjustment is referred to as the triennial “update."

Recognized Valuation

Computation used to alleviate the reappraisal phantom revenue effects in the state foundation formula of an increase in a district’s valuation due to an update or reappraisal. The recognized valuation adjustment adds, for foundation formula purposes only, one-third of a reappraisal increase to the district’s valuation in the first year, two-thirds in the second year and the full increase in the third year.

Renewal Levy

Voter approval to extend the term of a limited levy when it expires. The renewal levy must state the same purpose as the original levy. The effective rate of the renewal begins from the point where the original levy ends. A renewal levy proposal can combine with a proposal to raise additional millage.

Replacement Levy

Like a renewal levy in that it seeks voter approval to extend the term of a limited levy when it expires. Replacement levies differ from renewal levies because the replacement begins with an effective rate equal to the original effective rate of the levy which it replaces. In this way, a replacement levy allows a district to obtain the benefit of growth in the real property tax since the approval of the replaced levy. Replacement levies cannot be used for an emergency levy and cannot be combined with other changes in millage in a single proposed levy.

School District Income Tax (SDIT)

Limited or continuing levy proposed as a percentage rate on the income of district residents as reported for state income tax purposes. SDIT can be proposed in combination with a reduction in property tax. Because the SDIT taxes income, not property, there is no reduction factor involved, allowing unlimited growth in the proceeds. School district income taxes apply only to personal income and do not apply to the net profits of corporations.

School District Purpose

Legally defined reason for seeking a levy. Currently includes: operating expenses; specific permanent improvements and/or class of improvements; general, ongoing improvements; recreational purposes; community centers; support for public libraries or community centers; and the purchase of educational technology.

State Share Index

A calculation that takes into account the property wealth and the income of the residents of the district. The state share index is applied to the base formula amount to determine per pupil state funding.

Substitute Levy

A levy that is essentially a continuation or renewal of the Emergency Levy previously approved by voters with the exception that it can capture new revenue when new homes and new business/industry building are built in the District.

Tangible Personal Property (TPP)

Machinery, equipment and inventory used by business in the manufacture and/or sale of their products that is subject to taxation under a property tax. This class of property is also referred to as business tangible property. This tax has been completely be phased out.

Valuation of a School District

Taxable value of all Class I and Class II real property, general tangible personal property and public utility personal property in a district.

Valuation Index

A component of the state funding formula that compares the district three year average property valuation per pupil to the statewide three year average property valuation per pupil.

Valuation Per Pupil

Computation derived by dividing a district’s ADM into the district’s assessed valuation.

Wealth Index

For school districts whose valuation index is greater than their income index and their median income index is less than or equal to 1.5, the wealth index will be a combination of the valuation index at 60% strength and the income index at 40% strength. For all other school districts, the wealth index will be the same as the valuation index.

Weighted Funding

Method of funding certain categorical programs. Under this approach, pupils with special needs count as some additional multiple of one in the computation of the cost of an adequate education. The weight assigned to each pupil with a special need corresponds to an estimate of the additional cost associated with providing pupils with that special need an adequate education.

Property Tax

-

Local property taxes are taxes paid based upon land and building valuation located within the school district. Every owner of private and business property, including public utilities, must pay these taxes. County Auditors assess real estate taxes based upon 35% of the market value of a property. For example, an assessment of tax on property valued at $100,000 equates to $35,000 ($100,000 x .35 = $35,000). The measurement or rate of local property tax is a mill. A mill is one thousandth of a dollar. According to the Ohio constitution, all local governments combined can levy only 10 mills without a vote of the people. Un-voted millage, or inside millage are inside the 10-mill limitation. Counties, school districts, municipalities, and/or townships of each taxing district divide the inside millage, of which Beavercreek has 5.6 inside mills. Voters must approve all mills in excess of 10 mills. Millage in excess of the 10 mills, known as voted millage, or outside millage, cannot be collected without a majority vote from the voters in that specific district or community.

-

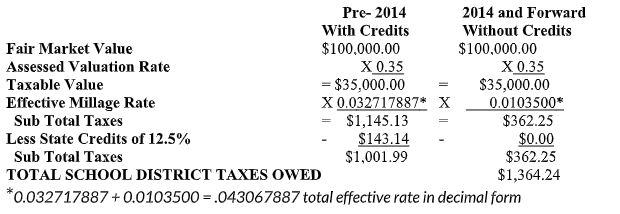

Residential taxes are calculated by multiplying the market value of a homeowner’s property by the assessed valuations rate of 35 percent and then the effective millage rate of the school district of 43.067887 expressed in decimal form of .043067887. The state of Ohio applied homestead and rollback credits of 12.5% to voted millage tax rates prior to 2014. Voted millage in 2014 and after no longer receive that credit. The following table demonstrates the calculation of the cost of school district taxes for $100,000 of property valuation in the Beavercreek City School District for tax year 2022, collected in calendar year 2023.

This cost per $100,000 valuation equates to approximately $3,410.60 in school district tax liability for a property valued at $250,000 ($1,364.24 x 2.5 = $3,410.60). Property taxes are an integral component of the revenue received by Beavercreek City School District. Understanding the basics of property taxes is vital as a member of the Beavercreek community. The information provided above has addressed broad questions and provides the reader with a general reference material as to how school district property taxes affect their individual real property tax liability. Reference

Materials Used: Greene County Auditor / Ohio Department of Taxation

-

House Bill 920, passed into law in 1976, limits the inflationary income of voted millage. County auditors reduce property tax millage correspondingly so that the real property tax of the average homeowner does not increase due to increased property valuation. This process creates a reduced tax rate or an effective millage rate that is less than the voted millage rate. The opposite occurs when property valuations decrease, the effective tax rate may increase to collect the original amount of tax passed by the voters. The County auditor’s annual evaluation process has reduced the district’s voted millage rate. While Beavercreek City School District has a voted tax rate of 54.47 mills, residents only pay 43.067 effective mills on their property for school district taxes.

-

As previously stated, House Bill 920 restricts Ohio schools ability to collect inflationary increases on voted taxes. Voted mills are the major source of income for our district as it is in most school districts. House Bill 920 freezes a school district’s income on voted mills. As inflation increases property valuations and operating costs for schools, a school district’s revenue remains the same. Revenue increases will not occur for schools, except as a one-time increase for new construction and a small amount of revenue growth on inside mills. With income on voted mills frozen, schools continue to ask to the local taxpayers for additional operating funds.